Price Factors

The way lenders determine mortgage interest rate pricing is something of a mystery to most people. Hopefully, we can shed some light on the subject.

There are 3 main factors that go into determining the pricing of your interest rate:

1) Your credit score.

2) Property loan to value (also known as LTV and / or equity).

3) The current market for the 10 Treasury bond price / yield.

Credit score and loan to value.

When a lender is determining the pricing for your mortgage rate, your credit score and down payment / loan to value play a very important role. If you and your neighbor go to the exact same lender, with the exact same loan amount, and lock in your rate at the exact same time, your credit score and loan to value will determine whether you have to pay more money, or less money, for the exact same interest rate.

Regarding mortgages, all interest rate pricing adjustments are based on risk. (By risk, we are referring to the risk of a borrower defaulting on a mortgage loan.) The higher your credit score is, the lower the risk you are in the eyes of your mortgage provider. The reasoning here is, if your credit score is high, that’s because you tend to pay your bills on time and you’re not “maxed out” on your credit cards. To any mortgage provider, that simply means you’re more likely to also pay your mortgage on time, since that’s what you tend to do with all your other credit liabilities. Similarly, the greater down payment you have (in the case of a refinance it would mean the more equity you have in your home) the lower your loan to value is, therefore reducing the risk of default. Your mortgage provider reasons that if you’re contributing a large down payment, or if you have a lot of equity in your home, you’re far less likely to walk away and let the property go into default than someone who has little to no equity in his or her home. So if your credit score is low, and/or your loan to value (LTV) is too high, a mortgage lender will see you as more of a risk. Much like how an insurance company handles their risky insurance policies, a mortgage lender will want to make more money on a riskier loan to offset the greater probability of a person defaulting on his or her mortgage. The higher the risk, the higher the cost for any given interest rate, the lower the risk, the less you will pay for your interest rate.

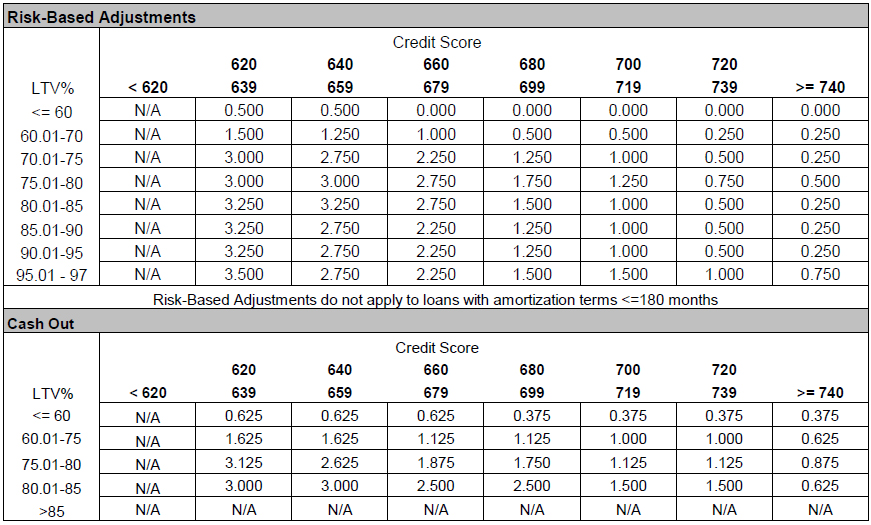

See grid below. (Please note: not every lender uses this exact same grid to determine their pricing guidelines. This is just an estimate of how a mortgage provider will determine the pricing adjustments on the home loans they sell. Some lenders will use this exact pricing, while others will use a similar grid for their adjustments.)

As you can see, a borrower with a 720 mid fico score and 70% LTV (30% down / equity) will pay only a 0.25% add on to the price of his or her interest rate. In contrast, a borrower with a 640 middle credit score and 80% LTV (20% down / equity) will pay 3.00% for the exact same rate as the 720 fico/70% LTV borrower. That’s an extra 2.75% price adjustment. (On a loan amount of $400,000, you’d be looking at a difference in cost of $11,000.) Of course, rather than pay an additional $11,000 for a mortgage, most borrowers would simply take a higher interest rate to lower the expense of his or her loan. Your fico score and LTV only determine the risk adjustments added to your rate pricing. What determines the base pricing of mortgage interest rates to begin with?

Market conditions. The 10 Year Treasury bond.

This is perhaps the most influential and least understood variable when it comes to determining the cost of mortgage interest rates. Mortgage pricing changes daily, sometimes two or three times in one day, depending on market volatility. Similar to how the price of a gallon of gas changes every day, mortgage rates prices are also in a constant state of flux.

So what controls the pricing on interest rates for home loans? The 10 year Treasury bond is used to set long-term residential mortgage interest rates (30, 25, 20 and 15 fixed interest mortgage rates). When yields rise on the 10 year T-bond, pricing on mortgage interest rates follow by rising as well. When yields fall, pricing on home loans also fall. This next part gets a little complicated. Bond yields and bond prices have in inverse relationship. So when bond prices go down, bond yields rise, and when bond prices go up, bond yields are dropping.

By keeping an eye on the 10 year Treasury bond market, you could gain some added insight with respect to current directional trends for mortgage pricing.